Buying a home is one of the biggest financial decisions most people make. Understanding how a mortgage works — and what determines your monthly payments — can help you make smarter, more confident choices when applying for a loan.

In this article, we’ll explain what a mortgage is, how interest and loan terms affect your payments, and how you can quickly calculate your estimated costs using our free Mortgage Calculator.

A mortgage is a long-term loan provided by a bank or lender to help you buy real estate. You agree to repay the borrowed amount, plus interest, over a set period — usually 15, 20, or 30 years.

Each monthly payment you make goes toward both:

Principal – the amount you borrowed

Interest – the cost of borrowing money

Your home serves as collateral, meaning if you fail to make payments, the lender has the right to take ownership of the property through foreclosure.

When it comes to mortgage costs, several key factors play a role in determining how much you’ll pay each month:

The larger the amount you borrow, the higher your monthly payments will be. A larger down payment reduces your principal and can lower your long-term interest costs.

Even a small change in your interest rate can significantly affect your monthly payments and the total amount you pay over the life of your loan.

Shorter loan terms (like 15 years) come with higher monthly payments but lower total interest. Longer terms (like 30 years) have smaller payments but higher total costs.

A higher credit score can help you qualify for better rates, potentially saving you thousands of dollars over the duration of your mortgage.

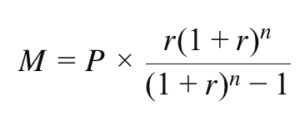

You can estimate your monthly payments using this formula:

Where:

M = Monthly Payment

P = Loan Amount

r = Monthly Interest Rate

n = Total Number of Payments

Of course, doing this manually can be complicated — that’s why we’ve built an easy-to-use, accurate tool for you.

👉 Try our free Mortgage Calculator to instantly see your monthly payments, total interest, and total cost.

A Mortgage Calculator helps you:

Plan your budget before applying for a loan,

Compare multiple loan options,

See how interest rates or loan terms change your payments,

Avoid surprises when signing your mortgage agreement.

By testing different scenarios — for example, adjusting the loan amount or down payment — you can make better financial decisions.

A mortgage is more than just a loan — it’s a long-term commitment that affects your overall financial health. Using our tools and guides, you can take control of your home financing journey.

Start by estimating your monthly payments with our Mortgage Calculator and explore more helpful tools on our Financial Calculators page.

You’ll need your loan amount, interest rate, loan term, and optionally a down payment.

Yes — you can enter your remaining balance and new loan terms.

No, but you can estimate them separately based on your local property tax rates.