Modified Duration measures the percentage change in a bond’s price for a 1% (100 basis point) change in yield.

It is derived directly from Macaulay Duration and incorporates the bond’s yield-to-maturity (YTM) to estimate interest-rate sensitivity.

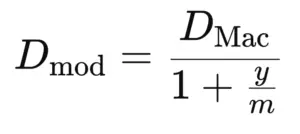

The formula is:

Where:

y = bond’s yield to maturity

m = compounding frequency (e.g., annual, semi-annual, quarterly)

If a bond has a Modified Duration of 7, then a 1% increase in yield will cause the bond’s price to fall by approximately 7%.

Conversely, a 1% decrease in yield will increase the bond’s price by roughly 7%.

It is a direct, intuitive measure of risk — the higher the Modified Duration, the more volatile the bond.